How Blockchain Technology is Revolutionizing Global Trade

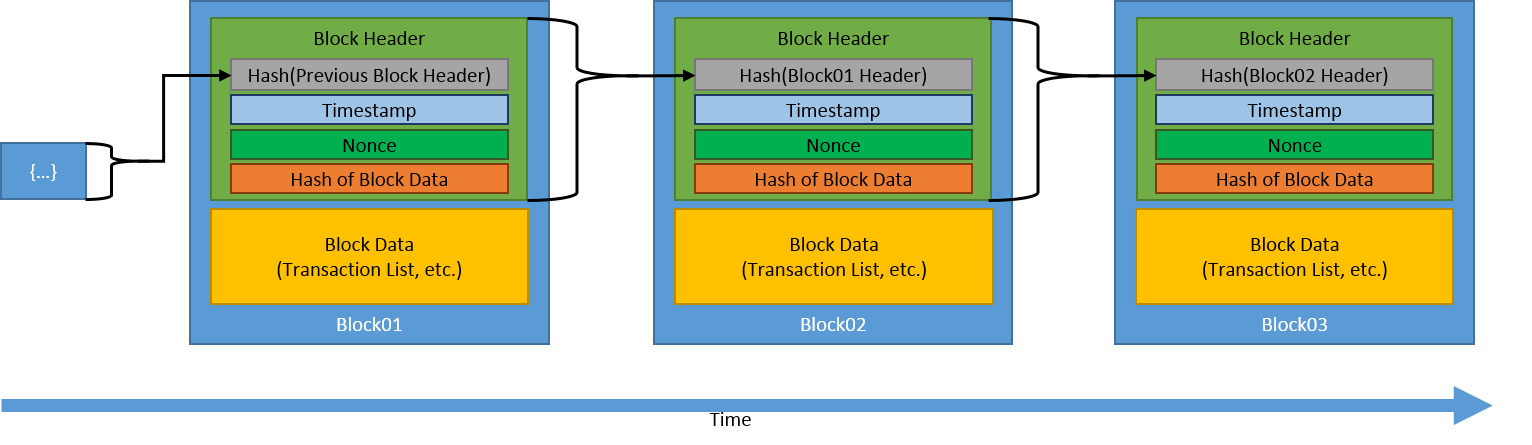

Blockchain technology is fundamentally transforming global trade by enhancing transparency, security, and efficiency in transactions. This decentralized system allows multiple parties involved in a trade to access and verify the same information without the need for a central authority. As a result, issues related to fraud, errors, and disputes are significantly reduced. According to a report by McKinsey & Company, integrating blockchain can reduce trade transaction costs by up to 30%, making it a game-changer for businesses engaged in international trade.

Moreover, blockchain's ability to streamline supply chain management has a far-reaching impact on global trade. With increased traceability, parties can track the journey of products from origin to destination, minimizing risks associated with counterfeiting and ensuring compliance with regulations. The World Economic Forum has reported that implementing blockchain in supply chains could increase global GDP by as much as $1 trillion by 2025. This level of innovation is fostering trust among stakeholders, which is essential for successful and sustained global trade relationships.

The Role of Smart Contracts in Shaping Tomorrow's Economy

Smart contracts are transforming traditional economic frameworks by automating and securing transactions in various industries. These self-executing contracts, written in code and stored on a blockchain, eliminate the need for intermediaries, reducing costs and increasing efficiency. According to Forbes, the ability of smart contracts to execute automatically when predetermined conditions are met creates a trustless environment, where parties can engage in transactions confidently. This innovation fosters a new wave of decentralization, paving the way for peer-to-peer interactions that could reshape everything from real estate to supply chain management.

As the demand for transparency and security grows in today's economy, smart contracts are poised to play a crucial role. They not only enhance trust among stakeholders but also enable novel business models, such as decentralized finance (DeFi). A report from McKinsey indicates that by utilizing smart contracts, businesses can streamline operations, minimize fraud, and innovate their services rapidly. As industries begin to adopt this technology at scale, it is vital to understand how smart contracts will further facilitate automation and efficiency, setting the stage for a more resilient global economy.

What is Decentralization and Why Does it Matter for the Future?

Decentralization refers to the distribution of authority, control, and decision-making away from a centralized entity. In traditional systems, power is often concentrated in one location or one governing body, which can lead to inefficiencies, corruption, and a lack of transparency. Conversely, decentralized structures enable greater participation, fostering innovation and resilience. Technologies like blockchain are pivotal in this shift, allowing for secure and transparent transactions without the need for intermediaries. For more about blockchain and decentralization, visit Investopedia.

Understanding why decentralization matters for the future is crucial. As society increasingly shifts towards digital platforms, decentralization offers a pathway to empower individuals, enhance privacy, and mitigate systemic risks. By redistributing power, we can create more equitable systems, whether in finance, governance, or social structures. For instance, decentralized finance (DeFi) allows individuals to access services without traditional banking intermediaries, promoting financial inclusivity. Explore the potential of decentralized systems further at Forbes.